FLOQ Finds Momentum ₿, AgriAku Refocuses 🌾, JumpStart Scales Up 🏗️

Dear subscriber,

Hi everyone, hope this finds you well. This week, Indonesia’s tech ecosystem delivered another strong mix of funding activity, strategic acquisitions, regulatory developments, and AI-related momentum. From FLOQ’s latest raise and Grab’s continued commitment to the market, to NVIDIA’s growing interest in Indonesia’s AI infrastructure ambitions, the signals point to an ecosystem that continues to attract attention from both regional and global players. We’re also seeing encouraging signs of consolidation and capital formation, suggesting that the market is becoming more mature, efficient, and investable. Let’s dive into the stories shaping the week.

Thanks for reading RISE by DailySocial!

Stay ahead,

DailySocial Team

🚨 What’s New

FLOQ Raises $11M: Regulated Crypto Gets Its Moment Indonesian crypto platform FLOQ has closed an $11 million funding round, a signal that investor appetite for regulated crypto infrastructure in the archipelago is finding its footing again. The raise comes as digital asset trading volumes across Southeast Asia accelerate, with Indonesia sitting on one of the region’s largest retail crypto user bases. FLOQ’s positioning as a compliant, regulated platform puts it well ahead of the curve as OJK tightens its digital asset oversight framework. For allocators, this round confirms that capital is still moving into Indonesian fintech verticals with clear regulatory footing.

JumpStart Series C: Vending Machines Are Serious Infrastructure Now Smart vending machine operator JumpStart has secured Series C funding from Cool Japan Fund, adding fresh capital to a network that already spans more than 6,500 machines across Indonesia and posted 200% financial growth in 2025. The investment will go toward expanding its AI-powered operations, deepening cashless payment infrastructure, and broadening product variety with Japanese brand partners. JumpStart’s model sits at a compelling intersection of automated retail, Japan-Indonesia trade flows, and the growing middle-class appetite for imported consumer goods. For investors tracking Indonesia’s physical retail layer, this is evidence that the segment is attracting cross-border institutional conviction.

Grab Bets Bigger on Superbank Grab has deepened its stake in PT Super Bank Indonesia to a combined 23.5% through coordinated purchases by GXS Bank and A5-DB Holdings, both Grab affiliates. The move signals Grab’s ongoing commitment to building an embedded financial services layer within its super-app ecosystem in the country. Superbank is a key vehicle for Grab’s ambitions to serve the underbanked segments of Indonesia’s 270 million population. As digital banking competition intensifies, a strengthened Grab-Superbank relationship positions both entities well ahead of the next wave of financial inclusion growth.

Alpha JWC Targets $300M Fund V, Danantara Gets Its BBB Alpha JWC Ventures is targeting up to $300 million for its fifth flagship fund. In the same week, both Fitch and S&P assigned a BBB investment-grade rating to Danantara Investment Management’s proposed global MTN programme, opening the sovereign wealth fund’s path into international debt markets. The dual signal, a leading regional VC raising fresh capital and Indonesia’s sovereign vehicle gaining global credit credibility, speaks to the deepening maturity of the ecosystem’s capital stack. Taken together, they suggest the country’s investment infrastructure is becoming increasingly legible to global allocators.

AgriAku Raises Bridge Capital, Bets on Fertiliser Focus Indonesian agritech startup AgriAku has raised approximately $4 to $6 million through a convertible note round led by Redbadge Pacific, as it sharpens its model around agricultural input distribution and steps back from a broader marketplace approach. The company, which previously raised $46 million in equity, is concentrating on fertilisers and farming inputs where demand visibility and unit economics are more predictable. The fresh capital extends runway while operational realignment continues. With Indonesia among the world’s largest agricultural producers, investors are willing to back focused, disciplined operators through the transition rather than exit the sector entirely.

👏 What’s Exciting

Indonesia’s E-Commerce Rules Get a Real Upgrade Indonesia’s Minister of Trade has signed a revised e-commerce regulation (Permendag PMSE), replacing the 2023 framework with five upgraded pillars: greater visibility for local and SME products, mandatory business licensing for all sellers, transparent platform fee and promotion policies, strengthened consumer protection, and governance of digital technology. The revision also formally brings ride-hailing platforms and online travel agents under the e-commerce regulatory perimeter for the first time, closing a long-standing definitional gap. For local brands and UMKM operators, the new framework creates clearer pathways to access government programs covering training, financing, and promotional support. Investors in consumer-facing digital businesses should read this as a regulatory environment becoming more structured, more predictable, and ultimately more investable.

Peak XV Trims Surge, Keeps the Conviction Peak XV Partners is restructuring its Surge accelerator, integrating it more closely with the firm's broader early-stage investing platform as it adapts to a changing venture landscape. Despite the changes, the firm is doubling down on its commitment to seed-stage founders, with Surge now able to invest up to $5 million per company. The move reflects a broader recalibration across venture capital, where firms are prioritizing focused support and higher-conviction bets over scale for scale’s sake. For founders, the message is clear: the model may be evolving, but access to capital and platform support remains firmly in place.

NVIDIA Calls Out Indonesia. That Matters. NVIDIA and Indosat Ooredoo Hutchison are poised to deepen their partnership as Indonesia positions itself as a rising AI infrastructure hub in Southeast Asia, with Indosat earning a rare mention in Jensen Huang’s keynote at GTC Taipei. The signal from the world’s most valuable semiconductor company carries weight: Indonesia is increasingly part of the global AI infrastructure conversation, not merely a market to be served. Indosat’s national telco footprint makes it a natural anchor partner for data center and AI compute buildout across the archipelago. For investors tracking the AI infrastructure layer in emerging markets, this partnership is one to follow closely.

Telkom Goes from 67 Subsidiaries to 19. The Leaner Version Will Be More Investable. State-controlled Telkom Indonesia is consolidating its structure from 67 subsidiaries down to 19 by year-end through a combination of mergers, divestments, liquidations, and a new holding arrangement, under Danantara’s directive. The move is part of the broader national program to reduce Indonesia’s state-owned enterprise count from over 1,000 entities to between 200 and 300, with the goal of sharpening business focus and strengthening competitiveness in the digital industry. For Telkom, the restructuring creates the conditions for a leaner, more strategically coherent digital infrastructure group. From an investor lens, the emerging portfolio of focused Telkom subsidiaries, particularly those in data centers and digital services, may become more attractive as standalone investment targets post-consolidation.

Grab Is Not Leaving Indonesia Grab has publicly dismissed circulating rumors of a potential Indonesia exit, reaffirming the market as a core pillar of its regional strategy. The denial comes as the super-app continues to expand its financial services footprint through Superbank alongside its ride-hailing and logistics operations. Indonesia remains Grab’s largest market by population addressability, with significant headroom in tier 2 and tier 3 cities yet to be fully captured. The reaffirmation, paired with continued capital deployment, suggests exit speculation significantly underestimates the strategic value Grab places on its Indonesian position.

🚀 What’s Next: SEA’s Deal Market Is Stabilising, and Indonesia Is in the Mix

After two years of contraction, Southeast Asia’s private capital market is showing its first credible signs of recovery. Startup funding rebounded sharply to $3.51 billion in H2 2025 from $1.86 billion in H1, while the region minted four unicorns in the year, up from just one in 2024. On the M&A side, ASEAN markets closed 375 transactions totalling $13.6 billion between September 2025 and February 2026, with Indonesia ranking among the three most active markets (by deal value) alongside Singapore and Vietnam. Indonesia’s deal activity included a $570 million cross-border acquisition of PT Sampoerna Agro Tbk by a Singapore-registered buyer, confirming that international capital continues to move decisively into Indonesian assets when the sector conviction is clear. The recovery is not yet broad-based, but the direction of travel has shifted.

Indonesia’s Startup Layer Is Consolidating From Within

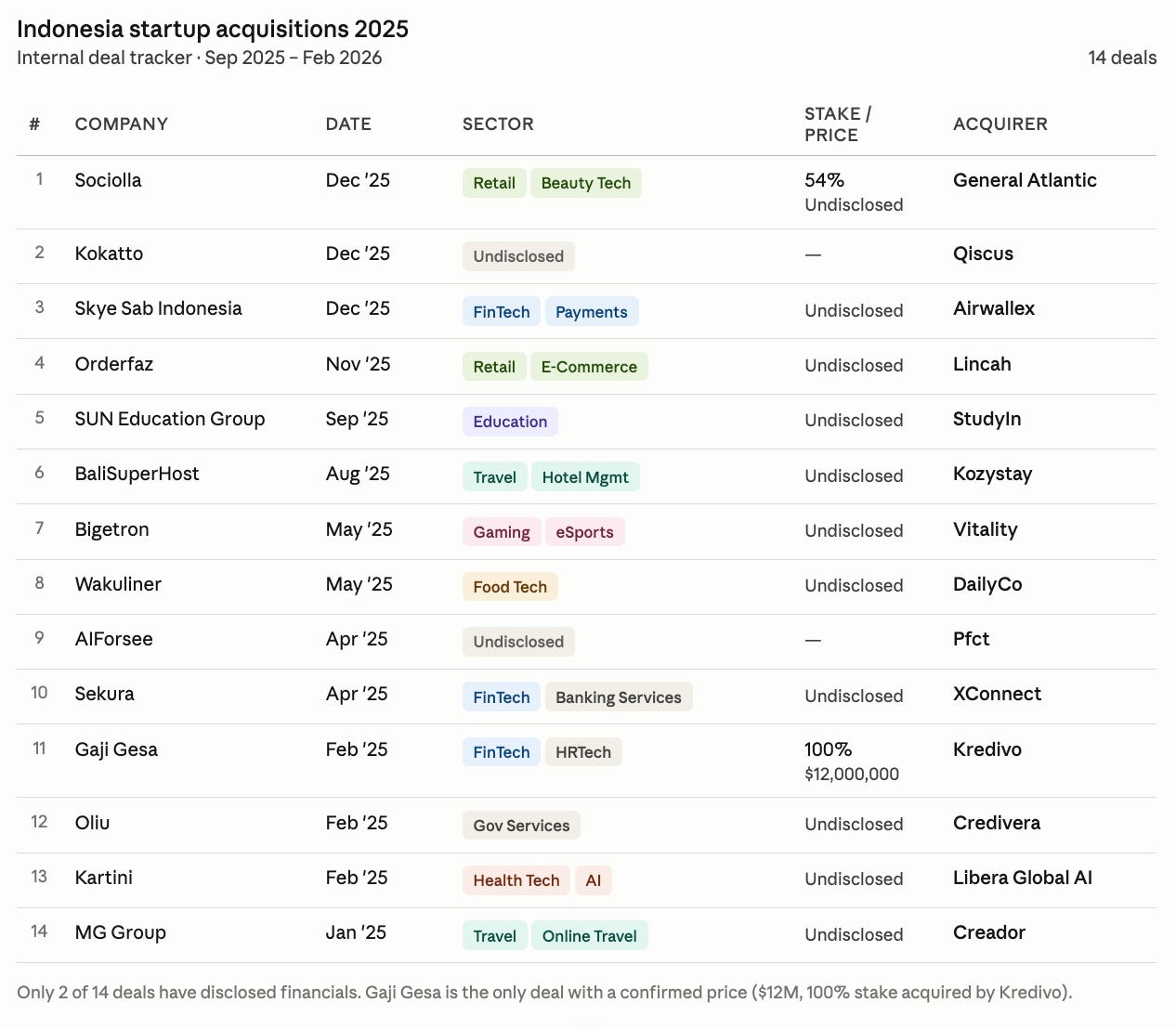

Below the PE headline numbers, a quieter but meaningful trend is taking shape at the startup and venture level. Indonesia recorded at least 14 startup acquisitions in 2025 across sectors including fintech, beauty tech, e-commerce enablement, food tech, health tech, and education. The fintech segment alone tells a coherent consolidation story: Kredivo acquired earned wage access platform Gaji Gesa outright for $12 million in February, adding an adjacent payroll product to its credit infrastructure. Airwallex, the global payments unicorn, acquired Skye Sab Indonesia in December, marking a direct entry into Indonesia’s payments layer through acquisition rather than organic build. General Atlantic took a 54% stake in Sociolla, one of Indonesia’s most established beauty commerce platforms, in the same month, bringing a global PE name into the consumer tech exit story. What this data reveals is a startup ecosystem that is beginning to produce exit-ready assets across multiple verticals, and an acquirer base that includes both domestic operators consolidating horizontally and international players entering via strategic acquisition.

The Outlook for 2026: More Dealmaking, Smarter Capital, Clearer Exit Paths

All three data layers point toward the same direction for 2026. EY’s Private Equity Pulse anticipates broader deal activity compared to 2025, with private credit emerging as an increasingly important financing layer for mid-market businesses. Conyers expects PE to remain active across digital infrastructure, healthcare, and consumer sectors through the remainder of the year. And at the startup level, Indonesia’s consolidation activity in 2025 suggests that the exit pathway, long considered the weakest link in the ecosystem, is beginning to function. Acquirers are showing up across deal sizes: from a $12 million HR-tech bolt-on to a multi-hundred-million beauty commerce stake. The data in this analysis skews toward PE and M&A by design, reflecting where institutional reporting is deepest. The VC and early-stage layer remains underreported in public data, but the consolidation activity at exit is the downstream evidence of what was seeded three to five years ago. Indonesia’s investment cycle is not stalled. It is maturing.