🧩SaaS leader Mekari acquires Desty. 🏆Sea Ltd back on top. 📈SEA’s fintech races toward US$1.1T.

Dear subscribers,

Indonesia ended the last week in horror as riots erupts across Indonesia driven by political demonstration that turned fatal. The whole weekend was a terrorizing one as riots spreads to smaller regions. Although most of the riots have died down, this week still starts in a rather fearful mood. We wish everyone safe and hope the situation improves soon for everyone

And now, this week’s highlights: funding (Pintarnya, Blitz, Kozystay), platform moves (Mekari, Amartha), and profitability signals (Wagely). Around the region, SeaLtd retakes the top spot by market cap, Atome scales profitably, and ZUZU raises to double-down on AI. Payment rails and rules continue to strengthen supporting Southeast Asia fintech’s march toward ~US$1.1T in 2025.

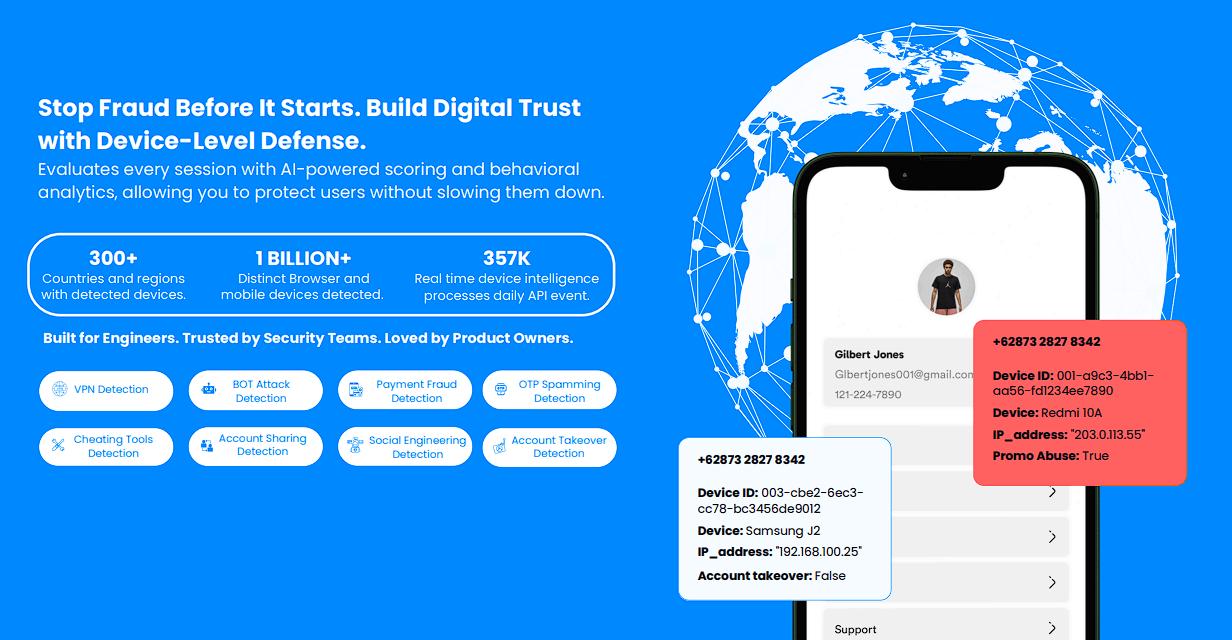

This week’s newsletter is sponsored by Keypaz, an advanced device-level fraud prevention system using fingerprinting, real-time monitoring, and AI risk scoring. Keypaz blocks high-risk devices across billions monitored globally, reducing operational costs, protecting brand reputation, and securing legitimate user experiences. [Try Now].

Keypaz, pioneer of proactive digital fraud defense!

Best regards,

The DailySocial Team

🚨 What’s New

Funding round-up (ID ecosystem):

Pintarnya, Indonesia’s jobs & worker-finance platform raised a US$16.7M Series A led by Square Peg, Vertex Ventures, and East Ventures to deepen its tech stack and expand worker financing. Traction to date: 10M+ job seekers, 40K+ employers, nearly 5× YoY revenue growth, breakeven targeted this year, and potential regional expansion. [Read more]

Blitz Electric Mobility, Indonesia-based EV logistics enabler closed Pre-Series A led by Vynn Capital with Iterative Capital and new investors including Balaji Srinivasan. In 2024: 3× revenue growth, 70% lower burn. Cumulative stats: 14M+ deliveries, 1,000+ e-motorbikes, 220M km traveled, operations in 30 cities. Indonesia’s courier market is projected to grow from US$7.86B (2025) to US$11.15B (2030). [Read more]

Kozystay acquires BaliSuperHost. Shortly after a Series A led by Integra Partners with Cercano Management and Intudo, Kozystay bought BaliSuperHost, the island’s largest premium villa operator. The combined group becomes Indonesia’s largest tech-enabled short-term rental manager with 1,000+ units across apartments, villas, and aparthotels. [Read more]

Mekari (Indonesia’s most valued SaaS startup) acquired Desty, an omnichannel commerce platform used by thousands of merchants. The move extends Mekari from back-office tools into integrated digital commerce—unifying inventory, orders, warehousing, products, finance, and customer comms in one system. Desty (founded 2021) adds landing pages, online stores, POS, and omnichannel orchestration. Expect faster merchant growth and stronger positioning as an end-to-end SME platform in Indonesia. [Read more]

Mekari and Desty founding team / Doc. Mekari Amartha becomes Amartha Financial Group (ID) to expand beyond micro-lending into payments and micro-investment to strengthen village-level economies (50,000 villages). With backers like IFC and Women’s World Banking, Amartha applies AI-based credit scoring from a decade of community data to deliver inclusive products distinct from urban-centric fintechs—while advancing financial literacy and inclusion for strategic segments such as women. [Read more]

Earned wage access platform Wagely reports full profitability, with US$120M+ disbursed across 3.5M transactions and loss rates <0.5%. With 200+ employers (incl. Adira Finance, BAT), Wagely serves 1M+ workers in Indonesia, positioning EWA as an employee benefit (not a loan) to drive recurring revenue. Beyond EWA, Wagely added savings and budgeting, and expanded in Bangladesh. Wagely sees room to apply generative AI for efficiency and worker financial literacy. [Read more]

👏 What’s Exciting

Sea Ltd. back at #1 by market cap (SEA)

Sea reclaimed the title of Southeast Asia’s most valuable public company at ~US$111B, edging past DBS (~US$110.3B) after a 300% rally fueled by Shopee outperformance. Cost discipline drove profitability; SPX Express logistics and digital finance are long-term levers. DBS also rallied ~65% on lending and wealth management strength but ceded the top spot.

Sea currently has a market capitalization of US$108.46n / Doc. Sea Atome Financial delivers profitable scale

2024 operating income: US$236M (+63% YoY); full-year profitability achieved. GMV >US$2B in 2024; by Q2’25, annualized GMV >US$4B and annualized net revenue >US$500M. Growth drivers: product diversification (insurance, savings) and the Atome PayLater Anywhere Card in the Philippines (1.5M cards issued by Jun ’25). Funding partners include BlackRock, EvolutionX, HSBC, DBS; gen-AI supports CX and credit ops.ZUZU Hospitality raises US$5.9M for AI

Series B+ US$5.9M led by Wavemaker Growth with Velocity Ventures and existing backers. Funds accelerate AI solutions, including RevMate, an AI revenue manager that dynamically adjusts rates using ZUZU’s multi-year price/occupancy dataset from 3,000 hotels. Early results: up to 40% efficiency gains and +25–30% revenue. Beyond pricing, AI helps respond empathetically to reviews and recommend ancillaries. With 200+ employees, ZUZU is expanding from small independents to regional chains.

🚀 What’s Next: SEA Fintech on Track for US$1.1T in 2025

Southeast Asia’s fintech market is projected to reach US$1.1 trillion in 2025, according to a report by fintech service company, UnaFinancial.

In 2024 it was estimated at US$907 billion, with digital payments and transfers accounting for nearly half of the total volume.

Digital commerce, digital banking, and digital investments followed, while digital lending and blockchain remained smaller contributors.

The study forecasts digital lending as the fastest-growing segment, rising 40.1% or about US$8.7 billion.

Digital payments are expected to grow 20.1%. Globally, Southeast Asia’s share of the fintech market increased from 1.4% in 2014 to 2.6% in 2024.

While East Asia remains ahead, Southeast Asia’s market is on an upward trajectory, underpinned by digital adoption and government support.

Several factors reinforce the region’s growth prospects: rising smartphone and internet penetration; the expansion of e-commerce that drives demand for digital payments; and the build-out of real-time and QR payment rails that lower transaction costs and broaden acceptance. On the regulatory front, financial inclusion initiatives—from sandboxes and licensing for digital banks and e-money to pushes for interoperability—are opening space for new products and business models.

Looking ahead, the opportunity remains sizable given the large unbanked/underbanked population and MSMEs, the wide SME financing gap, and growing demand for B2B payments solutions, embedded finance on consumer platforms, remittances, and cross-border transactions. Advances in AI and the use of alternative data are improving underwriting accuracy and fraud prevention, while bank–fintech collaboration and industry consolidation are helping with efficiency, trust, and scale. Taken together, these factors leave ample room for Southeast Asia’s fintech to keep growing.