Beyond the Blockchain

Why Bitcoin 3.0 really is Bitcoin 1.0

Over the past few months we’ve been bombarded with calls and visits from many leading financial institutions and other large global businesses, typically with the same questions: “Can you please explain to us what blockchains are?”, “What can blockchains do for our business?” or “How can we use the blockchain to dominate [insert industry here]?”. These questions are also typically followed by a not-so-friendly “We’re not interested in Bitcoin – only the blockchain.”

There is obviously a big need for education on the topics of blockchains and Bitcoin, so we thought we’d pull together some of the best resources we’ve come across together in one place to help everyone form their own opinions on this new technology.

At BitX we believe it is essential to continually challenge our own thinking and argue things from first principles. To that end, we also thought it would be a good opportunity to present our views on why we think the potential applications of ‘blockchain technology’ are very, very limited, and why many key decision-makers are placing the institutions they lead at a massive potential disadvantage by ignoring Bitcoin altogether.

So why is everyone getting so excited?

As far as fintech goes, 2015 was in many ways the ‘year of the blockchain’. This was driven by a number of factors including the acceleration of investment into blockchain companies by important financial institutions, their participation in blockchain consortiums, favourable regulatory rulings, and a barrage of positive press, including being featured on the cover of The Economist.

Most of these stories and initiatives perpetuate the popular view that the world has gone through some form of evolutionary process in terms of its understanding of this new technology: first discovering Bitcoin the ‘crypto-currency’, realising it has many potential flaws, and then digging deeper to discover the ‘technology’ behind it, the so-called blockchain or ‘Bitcoin 2.0’. It is this ‘blockchain technology’ that gets everyone really excited.

As one of the early pioneers in the crypto-currency industry, we have seen this evolutionary process before, and from experience we know that with enough time and understanding the rabbit hole goes even deeper, all the way to ‘Bitcoin 3.0’. However, ‘Bitcoin 3.0’ might not be what most people expect it to be.

We’ve seen this movie before

When we say we’ve been around the block, we really mean it. For those not familiar with our history, before we launched BitX, we were called ‘Switchless’ – the company that built the first fully-integrated crypto-currency system for a major multinational bank: an internal pilot for Africa’s largest bank, Standard Bank. This was all the way back in 2013, before most banks even knew what Bitcoin or a blockchain was.

While Standard Bank never launched the pilot to the public, we did manage to showcase our work at Finovate in London in early 2014, which led to an explosion of interest from large financial institutions and regulators all around the world.

We spent most of the rest of the year engaging with many of them – including some of the biggest banks in Southeast Asia, Europe, Australia and the US – helping them think about how best to apply this new technology to their business. More importantly, these engagements included not just looking at Bitcoin, but in-depth exploration of a variety of alternative protocols including Ripple, Ethereum and coloured coins. This experience gave us a first-hand perspective of the needs of these institutions and their customers, the unique challenges they face, and the practical opportunities and limitations of deploying these new technologies.

Despite being offered a lot of money to explore and implement some of these ‘blockchain’ ideas, our overall experience helped us decide to focus our time and energy in building an independent Bitcoin platform. This was driven by two major observations: firstly, that there is a lot of confusion to what blockchain technology actually is and what it can do, and secondly, that most of the dynamics around utilising blockchain technology doesn’t have anything to do with technology at all.

Let us explain.

So, what is a blockchain?

This can be a somewhat controversial subject, and depending on whom you ask, you may get a very different answer. But it’s really important to understand what the technology is before jumping to conclusions about what it can or cannot do.

Wikipedia somewhat narrowly defines a blockchain as ‘permissionless distributed database’. It expands on this definition by defining some of the basic principles and exploring various permutations. But blockchains are complex and mutating beasts, so for once Wikipedia might not be your friend. To really get a good understanding we suggest you lean on some of the work of the leading blockchain thinkers in the industry:

A good place to start is with Richard Gendal Brown, formerly with IBM and now with R3CEV, who digs a lot deeper in his excellent piece on understanding distributed ledgers from first principles. Richard’s blog also contains a treasure trove full of other excellent resources on the topic. Vitalik Buterin, Ethereum founder, makes an excellent contribution with his views on private vs. public blockchains and their potential strengths and weakness.

Next up: Simon Taylor, Barclays’s leading blockchain thinker, with his must-read article on 10 Things You Should Know About Blockchain. This includes references to the works of Gideon Greenspan of MultiChain, who builds on this by explaining how blockchains are different from normal databases and how to avoid a pointless blockchain bank project, indicating the set of conditions that need to be in place for a private blockchain to be most useful.

Tim Swanson provides some much-needed clarity on the limitations of using public blockchains for issuing digital assets in his piece on watermarked tokens. For those of you on holiday or sabbatical, William Mougayar does an excellent job of summarising the most relevant industry whitepapers, and there are further must-reads on some of the most exciting new initiatives like Sidechains, Interledger and Ethereum.

Not to be left behind, leading industry media player CoinDesk also provides some very useful references in their summary of stories that shaped the blockchain narrative in 2015, as well as their excellent quarterly State of Bitcoin report. There is also a plethora of other good materials available, including a great visual summary of the entire Bitcoin and Blockchain ecosystem by William Mougayar, his further exploration of the opportunities for financial institutions, another good ecosystem map here, and a deeper exploration of this broader ecosystem by Magister Advisors. Never leave McKinsey out of a good conversation – their latest contribution discusses the four stages of Blockchain adoption.

Many of these leading thinkers are also starting to view the word ‘blockchain’ as a slight misnomer, depending on the specific technology or application. Richard Brown suggests the term ‘replicated shared ledgers’ while Pascal Bouvier suggests more evolutionary concepts like ‘consensus computers’.

Confused? That’s okay – despite what others might make you believe, you’re probably in the 99%. It’s a technology that is still very new, with many people’s understanding of and views on the subject still changing on a monthly basis. The potential use of the technology also depends on who you are or what problem you are trying to solve, so in reality there is no one size fits all opportunity or solution here.

But despite all the moving parts, there are some things in life and in business that are still constant, and these are often around the non-technology aspects. So with all the hype and misunderstandings around blockchain technology it’s sometimes useful to take a step back and consider these factors.

Just to be clear, our vantage point is how do we use Bitcoin or blockchain technology to make it easier to move money, ultimately creating a society where money is frictionless and universally accessible. That said, many of our observations around the limitations of blockchain use cases extend beyond money or financial instruments, so even if you’re not interested in the ‘money’ use case only, we suggest you read on.

Blockchains are not just about technology

After spending a significant amount of time with many industry players on the subject, it quickly became apparent there was a lot more to consider than just the technology, so much so that we believe it is likely to affect the overall outcome of the industry. Some of our observations might seem very obvious, but we’ve been surprised at how much they are being ignored by people who should really consider them in making some very important decisions for them and the institutions they lead. Here are a few:

- You can’t have your toast buttered both ways. Two of the key benefits of a crypto-currency like Bitcoin is that it is interoperable and doesn’t require you to trust another counterparty. What many people fail to grasp is that by separating the ‘technology’ from the ‘crypto-currency’, the system loses many of these key characteristics. Some of these trade-offs have been explored and documented very eloquently by Richard Brown in his great piece on ‘Unbundling Trust’. While this article correctly demonstrates that the trade-offs are not binary and work more along a continuum, we would argue that the impact is a lot more severe than what most people realise. One important practical implication of all of this is that for existing industries, in most cases a ‘blockchain solution’ requires different parties to co-ordinate to ultimately reap the benefits of the technology.

- Co-ordination is tricky, if not impossible*. There is a reason that when the banks phone us they ask ‘What can a blockchain do for our bank’ rather than ‘what can a blockchain do for my industry’ – it might seem that we’re nit-picking on the choice of words, but it is a subtle yet very powerful reflection of the real intention of these project sponsors. They want to help themselves, not their competitors, and for a technology that requires large-scale cooperation, that makes all the difference.

We saw this first hand in our previous life as Switchless: in one instance we were working with some large banks to create a system to issue their own USD on a blockchain (let’s call it ‘Greencoin’) in order to better facilitate peer-to-peer trading with other banks. But in order for this to work, we needed the other banks we were dealing with to also accept Greencoin. But why would the other bank change their whole system to be standardised with their competitor? Why can’t they have their own token system – ‘Redcoin’ – that has all the nice modifications their institution wanted built into it? Where one starts with good intentions it very quickly degenerates into a massive coordination problem, exacerbated by parties that have long histories of being in competition with one another and used to being in control of everything they do. And no, it doesn’t matter if it’s tokens or shared databases or even a shared shuttle bus to the financial district, they still can’t work together.

*There are potential exceptions, but they are long shots. One solution would be to form a consortium that gives banks collective ownership of the project and additional economic upside for collaborating. In our view the only project that realistically seems to have a chance of succeeding with this is R3CEV, who have now signed up 42 banks. That said; don’t be fooled by the initial enthusiasm for a pilot versus actually pulling the trigger on a multi billion-dollar infrastructure makeover. It’s hard enough to get a bank to do one project like a mobile wallet within a two-year cycle, let alone something as significant as converting the entire organisation and industry to use blockchain technology. A lot of this activity is just driven by a misunderstanding of the technology and a general ‘fear of missing out’.

Another way such a standard can be enforced is through government or regulators, but after many conversations with various regulators it’s also quite clear that a realistic time horizon for this is so far out that open technologies like Bitcoin might already be unstoppable by the time it happens. One other interesting outcome could be that blockchain mania just scared everyone into action and coordination so much that it creates a self-fulfilling prophecy of people and institutions working together to rebuild the entire global financial system. But in that case blockchains might not be needed at all, and at its core it is still driven by these same human issues.

- Human incentives play a critical role in technology decisions. Key decision makers need to be incentivised to make the right long term decisions, and most of the time they are not, especially when the stakes are very high. We came across an interesting example of this while exploring building an interbank blockchain clearing mechanism back in 2014. It turns out a couple of banks, who shall not be named, wanted to build their own regional interbank clearing system to avoid using SWIFT or clearing through USD. The budget, technology and some initial co-ordination were all in place to get it done. The reason it didn’t happen was because the senior decision-makers in the banks were being treated to golfing holidays with some existing services providers – they just couldn’t be bothered to change the status quo in their lifetime. This is even more exacerbated when there is a share price to manage or pensions are tied to company performance. The mid-level innovation managers in the banks could jump around all they wanted; the key decision makers simply were not incentivised right – both on a personal and institutional level.

- Human beings are survivors. Not only are senior decision-makers not incentivised to co-ordinate or change things, but this is even more the case for hundreds of thousands of mid-level and junior staff spread across these institutions. A lot of what the blockchain promises is to optimise processes, eliminate reconciliations etc., much of which currently requires humans to do. These people are definitely not going to be working towards solutions that make themselves redundant, especially in these challenging global economic conditions. In fact, they will fight very hard against it.

- Can you really trust a blockchain? When value is represented on a blockchain, whether as a data entry or some form of token (we’ll just use the latter to explain the narrative easier, but the conclusion applies in most cases), you need to trust that the party that issued the token actually has ownership of the asset backing that token in the first place. This might seem like a very obvious thing, but we’ve been surprised at how many people still seem to think that by just ‘issuing it on the blockchain’ it somehow magically makes the counterparty risk for that asset disappear.

There are countless examples where things can and have gone wrong with this in real life, whether accidentally or fraudulently. This goes all the way from committing the wrong asset information to a database in the first place, to not having visibility on what the ‘trusted’ issuer does with the asset behind the scenes (e.g. ETF issuers lending out the underlying assets without the holders knowing it, exposing the asset to undisclosed counterparty risk). Having a ‘blockchain solution’ doesn’t mitigate most if any of these risks.

- Network effects will drive the agenda. Open protocols like Bitcoin allow for permissionless innovation and tend to have stronger network effects, and once they kick in they are incredibly difficult to stop. The implications of using open systems are well documented and we’re not going to go into more detail now, but it’s important to consider that many of these systems have qualities that are vastly superior to closed systems. There is a reason that the open internet we know today ‘beat’ other closed-loop systems in the early days of the web.

If you asked us two years ago which crypto-currency or technology would likely become the de facto standard, we would have told you ‘something like Bitcoin, but probably not Bitcoin’. After witnessing these network effects in action, we are now firmly in the ‘more than likely it will be Bitcoin’ camp.

- Speed is critical. Most financial institutions got away with not having to change during the on-going internet revolution, where entire industries have already been decimated and speed of execution has arguably become the most important competitive advantage for most organisations. But things are changing quickly and with barbarians at the gate, speed of execution is becoming more critical than ever in the financial services industry.

Unfortunately, with massive disadvantages due to legacy systems and assets, out-dated processes, uncompetitive cost bases and a lot of momentum (in the wrong direction), moving fast is always going to be challenging for the existing financial industry. More importantly, with organisational cultures that are not used to speed nor incentivised for it, we struggle to see how it is possible to turn these ships around. While in theory the banks can co-ordinate with some private blockchain solutions, it will take way too long to do so, and in our view, by that time open protocols or public blockchains like Bitcoin would have already built up too much momentum to stop.

- “A confused market doesn’t move”. These are some wise words once spoken to us by the leader of one of the most influential financial institutions in the world, and we observed it in reality over and over again. With all the new ‘blockchain’ solutions coming out, it’s becoming increasingly confusing for CTOs to make decisions around which technologies to use: Ripple, Ethereum, Sidechains, R3CEV, Bankchain, TRUST, Hyperledger, and even our own FALCON, to name but a few of the publicly disclosed alternatives. There is also a whole pipeline of new ones that will create even more confusion. There is no safe ‘buy IBM’ option, so we struggle to see any CTOs signing off on major blockchain projects in the foreseeable future.

- Go big or go home. Using the example of financial institutions collaborating, even if by some miracle all of them manage to co-ordinate, we still believe that in the bigger scheme of things, the impact will be marginal. Santander predicts that blockchain technology can save banks USD20bn a year by 2022. These numbers are a drop in the ocean compared to how much money banks will earn and spend on an annual basis by then, and even if the amount is much higher, will still dwarf in comparison to the profits that will be lost by competing with a new fully decentralised global currency.

- If it ain’t broke, don’t fix it. Many blockchain believers tout a whole range of apparent issues with the existing financial infrastructure. These include the susceptibility for tampering, reconciliation costs, a lack of transparency etc. But in practise, many of these issues are not nearly as big as people make them out to be – banks are not tampering at any material level (and have many existing checks to make sure this is the case), they have well-functioning settlement systems (even if they are old, they still work), and often cannot be more transparent for regulatory reasons. They might be able to do things a bit cheaper or more transparent with some form of blockchain technology, but to most of them the cost of replacing it vastly exceed the benefits.

- Square pegs in round holes. In many instances the most important question is whether blockchain technology is the most optimal tool to use to solve a specific problem. We recall a meeting with one of the largest banks in Europe where they excitedly told us about a new blockchain initiative where six of the largest banks were experimenting with blockchain technology that involved issuing securities on their own private blockchain and settling them between one another. We asked the project lead whether this was a pre-selected group of parties, and whether they already trusted one another. He confirmed it was the latter, after which we asked why they couldn’t just issue and clear it on a secure database – it should be faster, cheaper and safer than using a blockchain. He seemed confused for a while but once the reality of the situation dawned on him we could see the disappointment in his eyes – yes, since the parties had to trust each other, using a database was in fact the easiest solution. You’d think people would have caught on by now, but we’ve seen this scenario play out over and over again, all the way from hackathons to start-up pitches to meetings with large global institutions, across countries and industries.

This leads us to the very popular and never ending debate around whether modern databases are good enough, if not better, to do most things a blockchain is proposed to do. Like many things in life, it depends. While technically there are certainly some benefits to using blockchains, one still has to question whether they are material enough to make a difference, and more importantly, which use cases these apply to. The devil is in the detail with these things, and when you look at the conditions that need to be in place to really reap all the benefits of blockchain technology, the list becomes very short. So in most cases we would still argue that in practise a database could do the job better than a blockchain. Put it to the test – whenever someone tells you about building something using ‘blockchain technology’, first ask whether it would not make sense to rather build it on a normal database. You’ll be surprised.

Our view is certainly not the popular one, and some leading blockchain thinkers like Pascal Bouvier put forward some very good arguments on why Bitcoin might not be the technology to back. But there are also some blockchain supporters like Simon Taylor and Richard Brown that agree that the “Blockchain not Bitcoin” narrative is ignorant and that you should ignore Bitcoin at your own peril. Others like Gideon Greenspan have also weighed in on the Bitcoin vs. Blockchain debate with an excellent article on whether there is value in having a blockchain without a crypto-currency. Some initiatives aim to incorporate the best of both worlds, Sidechains leveraging Bitcoin as a core part of its infrastructure and Interledger using Bitcoin, amongst others protocols, to build a global payments standard. There is also a minority of the founders of some of the largest and best-funded Bitcoin companies in the world that have been quite outspoken on the topic: Circle founder Jeremy Allaire does a great piece on ‘the big bad B word’ and Xapo’s Wences Casares shares some of his views in a recent interview with CoinDesk.

Bitcoin 3.0 = Bitcoin 1.0

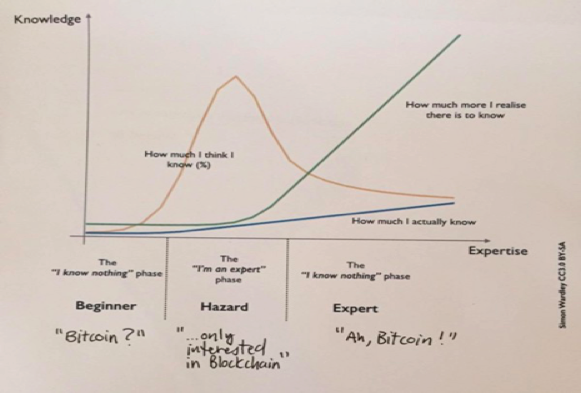

To many outsiders we seem stuck in the past – still doing ‘Bitcoin 1.0’ when everyone else has moved on to ‘Bitcoin 2.0’. We believe this is simply a temporary market dysfunction. In our view, the evolutionary process for crypto-currency is simply getting intrigued about Bitcoin, realising there is an underlying technology that is useful, but upon further investigation realising that the most useful and impactful application is actually still crypto-currency: Bitcoin 3.0.

We found this great picture to explain this phenomenon more visually. In essence this image shows how expertise is developed on any subject matter, and how one’s actual and perception of knowledge evolves with time. The image is meant to be applicable to any topic (in this case it was used to describe the venture capital industry), but we added the relevant Bitcoin vs. Blockchain labels. curve

There is a reason the smart money like Andreessen Horowitz invested significant capital in Bitcoin companies a long time ago and haven’t jumped on the whole blockchain bandwagon – because they have the experience and foresight to see this same market dynamic play out. And while there is a lot of talk about blockchain technology being the next big thing, most of the money invested into the sector is still going to Bitcoin companies. Follow the money, not the mouths.

So where to from here?

In conclusion, we are not saying that ‘blockchain technology’ (or some other form of permissionless distributed databases or decentralised applications) should be ignored, and that Bitcoin is the only way. It is worth spending time and resources looking into what these technologies have to offer, and in our view particular initiatives to watch out for are R3CEV, Ethereum, Sidechains and Interledger.

What we are saying is that one: it is important to form one’s own views and realise the difference between the theoretical benefits and practical limitations – that things like existing industry structure, timing and human incentives are all important, if not critical considerations – and two: that the market (and in particular financial institutions) is most certainly overvaluing the potential impact of ‘blockchain technology’, while severely undervaluing the concept of Bitcoin. As a consequence, it would be very irresponsible for any decision-maker in an organisation to ignore Bitcoin altogether.

But what about all the issues around Bitcoin? The bad reputation? The regulation? The blocksize debate? The mythical ‘killer app’? We’ll get into these topics in more detail in future posts, but the gist of it is that Bitcoin will enable companies like ours to build truly global ‘banks of the future’ at an unprecedented pace and with unrivaled economies of scale.

- This guest post is republished by author's permission. Original article was published in BitX blog.

Marcus Swanepoel is the co-founder and CEO of BitX. Previously, he worked for Standard Chartered in Singapore and before that 3i and Morgan Stanley in London. He holds an MBA from INSEAD, is a qualified Chartered Accountant and a CFA charterholder. He is a South African citizen and a Singapore Permanent Resident.

Sign up for our

newsletter

Review Order

Monthly

Rp 150.000

Payment Details

Subscribe Monthly

Total Payment

By clicking the payment method button, you are read and

agree to the

terms and conditions of Dailysocial.id