Indonesia to Realize Digital Bank Initiative in 2020

Several banks have plans with separate entities and new brands

We have witnessed various digital banking innovations in the last decade. Mobile and internet banking can be examples of banking digitalization that is most related to daily life. Thanks to this innovation, it is easier for customers to perform financial transactions.

Indonesian banks have also begun to explore service connectivity through the Open API strategy. The digital business growth in this country driven by e-commerce and fintech platforms and to be said as a driven factor for banks to develop these innovations. Currently, cross-platform transactions are very possible.

In recent years, fintech has played a significant role in providing access to efficient and practical financial services. Fintech managed to disrupt the traditional banking business model with a fast onboarding process.

Based on the 2019 Fintech Report, 79.9% of 747 respondents in Indonesia used digital wallet services, followed by investment (31.5%), paylater (30.9%), online multifinance (12%), insurtech (11, 8%), crowdfunding (8.2%), P2P lending (6.2%), and remittance (2.4%).

The role of fintech in the financial ecosystem has become a momentum for banks to innovate. Beyond its mobile banking services, a number of banks in Indonesia are very eager in developing digital financial products, both independent and through collaboration. Also, customers can now open savings accounts through mobile banking applications and digital platforms.

In the context of digitalization, the above efforts are certainly relevant to the demand of today's users. However, these are not enough in order to reach broader financial inclusion. The population of people who don't have access to financial services (unbanked) is quite large. The limited number of ATMs and branch offices are an obstacle for banks.

Google, Temasek, Bain & Company report in October 2019 noted that there were 92 million Indonesians in the unbanked segment (50.83%), followed by the banked segment at 42 million people (23.20%), and the underbanked segment 47 million (25.97%).

The Indonesian banking industry is aware of this phenomenon that today's financial products are not only monopolized by banks. This situation also indicates that banks have not been able to close the gap between the ones with financial literacy and those who are yet to aware of this, with the traditional business model.

Digital bank in Indonesia

After banking digitization, digital bank concept is currently trending in Indonesia. The effort shows banking digital transformation is no longer depend on service digitization, but also to become a separate entity.

In definite, digital banks are different from banking digitalization. Borrowing the current popular term, the concept of digital banks is generally referred to as neobank, which is popular since 2017. Also, quoting the words "Neo Bank and the Future of Retail Banking in Indonesia", the term digital bank is often defined as a challenger bank.

Challenger banks in the world have even acquired millions of customers. Some of them are Nubank (Brazil), Monzo (United Kingdom), N26 (Germany), and Chime (United States).

Back to the origin, digital bank or neobank is defined as a bank that operates online-based services without a physical branch office. Digital Bank offers easy access with a user-friendly UI/UX. With an internet connection and smartphone, anyone can open an account and access other financial services.

Digital banks also have the opportunity to be able to leverage the customer's journey through the development of financial support services and make their products a daily product for customers.

Of course the above concept is inversely proportional to traditional banks where financial services — even though there is already internet and mobile banking — still require face-to-face and physical branch offices. This is understandable considering that banks are a business of trust so physical contact is still needed.

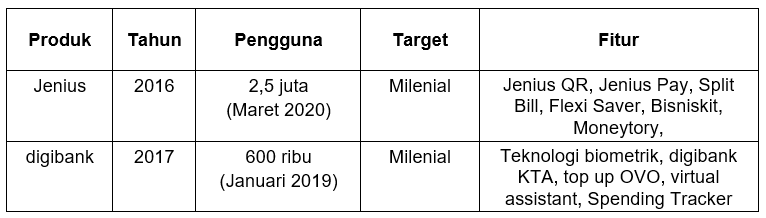

In Indonesia, digital banks are mostly linked to Jenius services (2016) and Digibank (2017). Both are often referred to as the pioneers of the first digital bank. However, there are also those who call it a spin-off product since both are still operating under BTPN and DBS Bank as its main entity.

Jenius and Digibank are examples of application-based services that offer basic banking products, namely savings, online account opening. Both also offer other supporting services, such as financial regulators.

If the root is on the expansion of financial inclusion, Jenius and his staff are considered not a digital bank. This is because both are targeting segments of society that already achieve digital literacy (digital savvy). Meanwhile, the unbanked segment tends not to understand financial literacy.

The next step for digital bank

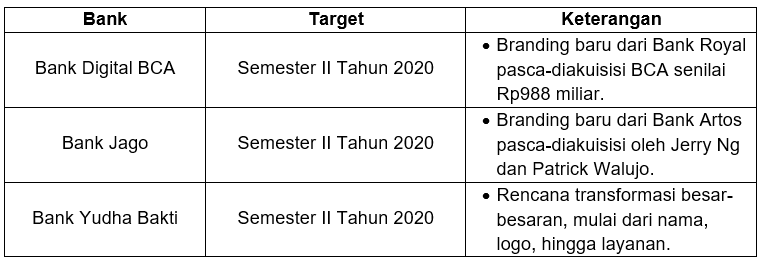

As the ecosystem and technology is getting mature, 2020 would likely to be the year of the digital banks realization in Indonesia. Some of the plans we have summarized, including Bank Digital BCA, Bank Jago, and Bank Yudha Bakti (BYB). Efforts to become a digital bank as a new entity have all been passed through the acquisition process.

Quoting Kontan, BCA has acquired Bank Royal worth Rp988 billion in 2019. Bank Royal will change its name to Bank Digital BCA targeting some realizations in the second-semester, 2020. The target market is retail and SME segments, different from the main portfolio of its parent company which mostly engaged to corporate. Bank Digital BCA already has a permit from OJK and is ready in infrastructure.

It is known, the company is currently preparing the P2P lending initiative for BCA Digital Bank. However, BCA's President Director, Jahja Setiaatmadja revealed that he is not to launch the service in the near future. "We wouldn't dare to enter P2P for the risks are enormous, we are still preparing," he said as quoted by Katadata.

Furthermore, Bank Artos officially changed its name to Bank Jago after acquired by its seniors, Jerry Ng and Patrick Walujo. According to Bank Jago's Managing Director, Kharim Siregar, his office is finalizing a business model and perfecting applications targeting to launch before the fourth quarter of 2020. Quoting Bisnis.com, Bank Jago will target the middle segment and mass-market. In addition, Bank Jago will also collaborate with digital platforms in various business verticals, such as e-commerce, ride-hailing, and P2P lending.

DailySocial has in touch with BCA and Bank Jago representations regarding the realization of this digital bank, but their team sre still reluctant to disclose any information. "Our directors are yet to confirm any information to the media because they are currently focusing on preparing applications and everything," Bank Jago's Senior Manager Nurul Kolbi said in a short message to DailySocial.

Unlike the two, Bank Yudha Bakti (BYB) started to be controlled by PT Akulaku Silvrr Indonesia which runs Akulaku's fintech services in 2019. Akulaku's entrance is expected to accelerate the digital transformation process of BYB, which is to become a digital bank without branch offices and develop mobile applications to increase market penetration.

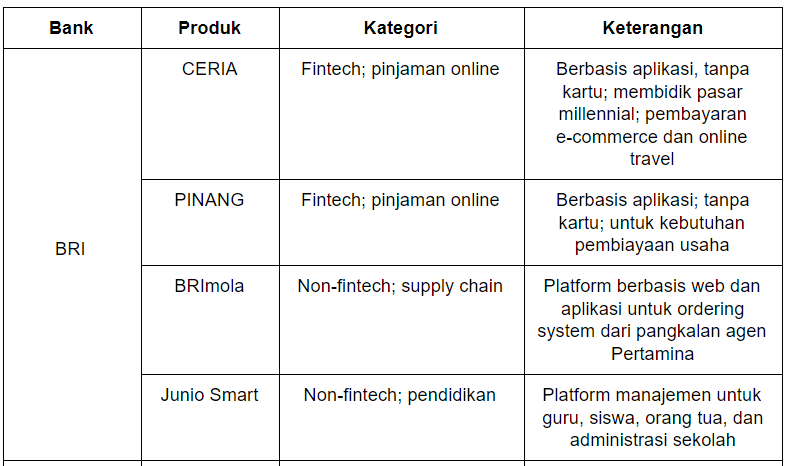

DailySocial also reached BRI's Indra Utoyo, Digital Director, Information Technology, and Operations regarding this matter. He commented, BRI did not perform a similar strategy with the above banks. However, BRI is considered to have made a major transformation to become a digital bank.

In order to become a digital bank, Indra ensured that BRI must maximize excellence in physical networks. "The winner is the one who can combine physical and digital excellence. Whatever the entity, both BRI, and its subsidiaries, must be a digital company. There is no need for a dichotomy between digital banks and non-digital banks," he said.

Without this dichotomy, he said, BRI has provided value from the concept of digital banks with digital-based banking services. BRI became the first bank to launch PINANG and Ceria digital lending products. Then, the first bank to provide account opening services with the entirely digital-based KYC process.

Indra emphasized that digital cannot replace trust, service, and brand. However, without digital, we cannot get all three. It means those with the 'digital' label do not necessarily translate into trusted banks than large banks that have transformed digitally.

"To date, I have not seen a successful digital bank or neobank in the world. For me, the winner is the one that combines physical superiority or human touch and digital. The term is phygital," he said.

Separately contacted, BTPN's Head of Digital Banking, Irwan Sutjipto Tisnabudi admitted that the emergence of a new digital bank would help create a digital financial ecosystem and encourage education for better financial literacy. In fact, this trend will bring many collaboration opportunities.

Regarding the possibility of Jenius becoming a separate entity, Irwan assured that Jenius currently still supports the BTPN business to expand the current market segments. He also emphasized the main strategy through co-creation and collaboration with like-minded partners to develop products that are relevant to customers.

"In carrying out digital transformation, BTPN believes that digital is the core of the business and value proposition, not an additional channel. Our priority is to build an ecosystem that supports life finance with a broader scope so that the benefits can reach the digital literacy people," he explained.

Jenius became the result of BTPN transformation which was developed through the process of creation and collaboration with thousands of digital-savvy for 18 months. As of March 2020, Jenius has secured more than 2.5 million users. The company has also just introduced the Bisniskit feature for new business owners and Moneytory to help with financial management.

Regulation and challenges

To date, digital banks still operate under the law of conventional banks. This is regulated in OJK Regulation Number 12 concerning Digital Banking Services Provided by Commercial Banks. There is no separate law to regulate the virtual account opening.

The regulation clearly states that digital banks are different from digital banking services (m-banking, SMS banking, e-banking, etc.). The difference is clear that all digital banking services can be accessed via smartphones.

Beyond that, digital banks cover all banking services from account administration, transaction authorization, financial management, and / or account opening/closing, digital transactions, and other financial product services based on OJK approval.

According to Bhima Yudistira, Institute for Development of Economics (Indef) observer, there is no need yet to draft new regulations to accommodate the law of digital banks. Moreover, existing regulations were only issued in 2018. However, Bhima highlighted that the government needs to pay attention to the high-security aspects and data utilization for third parties.

On the other hand, he also sees that the trend of digital banks is driving a new landscape of banking in the banking sector. According to him, banks that invest in digitalization will obtain a greater market share than banks that continue to operate conventionally.

"The demand for digital banking is greater along with the growth in the number of active internet users in 2020 reaching 175.4 million people. This means that banks are expected to provide faster services at affordable costs, and access anywhere, anytime," he said.

If a digital bank is realized, the impact will be very large, especially for millennials. However, it is not without obstacles that banks are also deemed necessary to conduct education for other market segments, such as SMEs and rural areas. "The important thing here is developing digital banks must run along with the penetration of internet network access to remote and outermost areas," Bhima said.

–Original article is in Indonesian, translated by Kristin Siagian

Sign up for our

newsletter

Review Order

Monthly

Rp 150.000

Payment Details

Subscribe Monthly

Total Payment

By clicking the payment method button, you are read and

agree to the

terms and conditions of Dailysocial.id